Insurance sector on growth trend

PETALING JAYA: Despite significant economic losses from the flooding last December, the general insurance and takaful sector has not been badly hit, says RAM Rating Services Bhd.

According to its co-head of financial institution ratings Sophia Lee, (pic) the overall impact of the floods on the sector is expected to be manageable, even as more claims come through in the first quarter of 2022 (1Q).

The net insured loss borne by general insurance players was estimated to be around RM1bil, which is a mere 16% of the aggregate RM6.1bil economic losses.

Lee told StarBiz that “this is due to the fact that many homes and vehicles in Malaysia are uninsured or underinsured against flood risks”.

The general insurance and takaful industry’s underwriting performance also improved in 2021.

Better claims experience – mainly from motor covers – lifted the underwriting margin of general players to 13% last year from 10% in 2020 and 6% in 2019.

The improvement would have been more significant if not for higher flood-related claims in December, she pointed out.

According to its co-head of financial institution ratings Sophia Lee, (pic) the overall impact of the floods on the sector is expected to be manageable, even as more claims come through in the first quarter of 2022 (1Q).

According to its co-head of financial institution ratings Sophia Lee, (pic) the overall impact of the floods on the sector is expected to be manageable, even as more claims come through in the first quarter of 2022 (1Q).

“From a claims perspective, the non-life sector still benefited from mobility restrictions last year (whether government or self-imposed). As we tread towards endemicity, claims could normalise as early as this year.

“Environmental experts warn that the frequency and severity of climate-related events such as extreme floods could intensify further, going forward.

“Greater awareness of the availability of flood and special perils (natural disasters) cover among households and businesses could shield them from the sudden impact of such events and help safeguard their financial well-being,” said Lee in RAM’s latest review of the sector.

RAM Ratings also maintained a stable outlook on the domestic insurance and takaful industry for 2022.

The fire class remained the second largest segment for general players after motor, accounting for 20% and 50% of aggregate general premiums and takaful contributions in 2021, respectively.

The non-life sector’s premiums and takaful contributions grew 4% to RM21.5bil last year (2020: 0%; 2019: 2%).

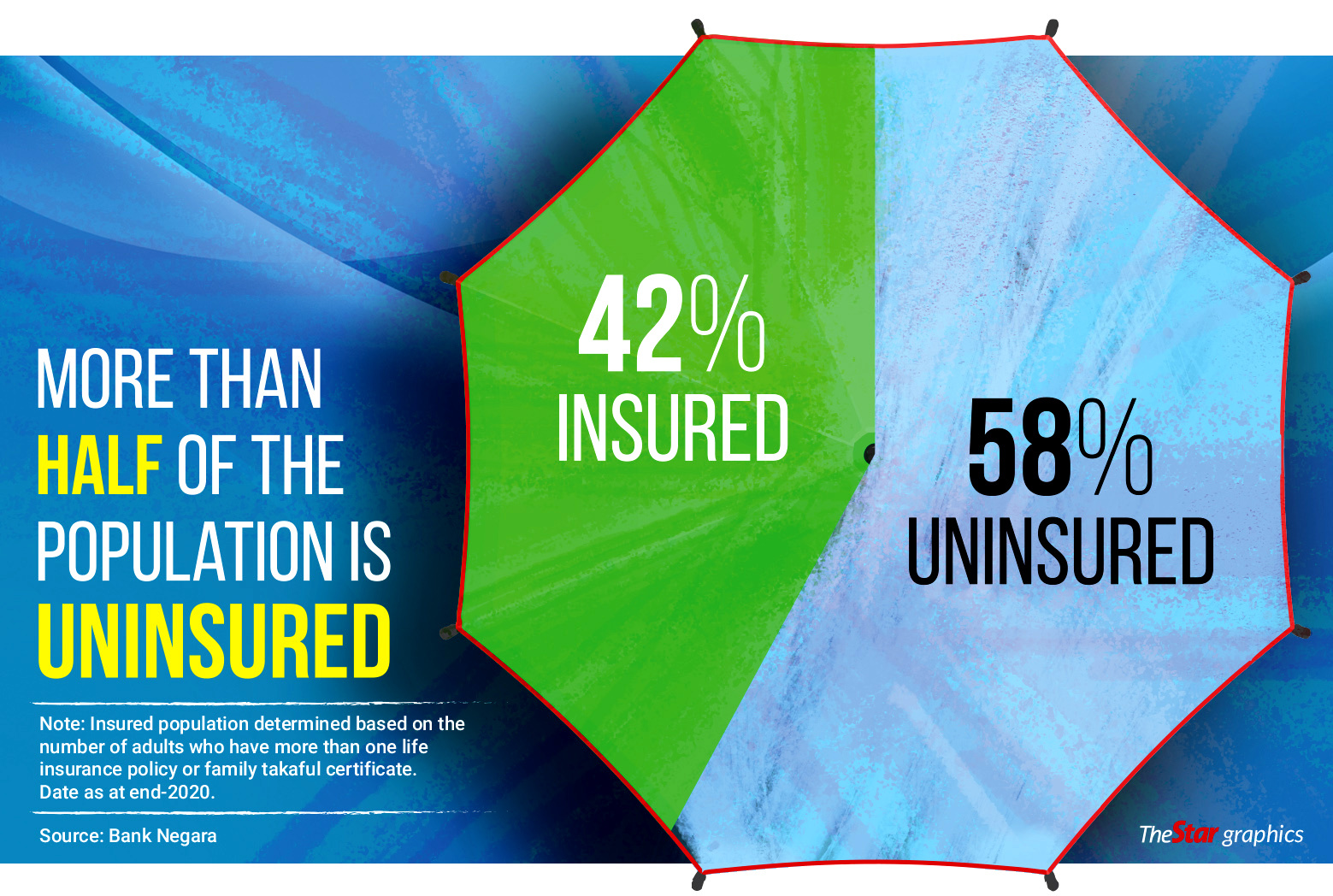

The absence or the lack of life and medical protection is also evident from Bank Negara’s statistics, which indicated that more than half the Malaysian population is uninsured, ie, does not own a life insurance or family takaful policy, RAM noted (see graphic).

To increase insurance penetration, the government has introduced several initiatives among the lower-income population, including MySalam and Perlindungan Tenang.

Thanks to the RM50 vouchers provided for the purchase of these policies, the number of new life and family takaful policies saw a sharp 46% jump in 2021 to three million policies, the rating agency noted.

However, as these are smaller ticket-sized in general, investment-linked plans continued to be the main growth driver in terms of new business (NB) premiums and contributions, RAM said.

“As inclusion is featured as one of the three value propositions that prospective digital insurers and takaful operators (DITOs) must have, digital insurance/takaful players will play a role in raising Malaysia’s insurance penetration rate,” Lee said.

The implementation of value-based intermediation for takaful (VBIT) framework to generate sustainable impact – which was introduced by the central bank in July 2021 – also features the inclusion agenda as a cornerstone, she noted.

Innovative propositions from the DITOs and existing insurtech players which will focus on the unserved and underserved are expected to reach out to segments less tapped by the traditional players, lending strength to efforts to be inclusive on the insurance protection front, RAM said.

Overall NB generation of the life and family takaful sector rebounded strongly to 12% and 29% respectively in 2021. In 2020, life insurance NB premiums contracted by 3%, while the family takaful saw a 7% growth.

As the sector rides the recovery wave, NB growth for life and family takaful players could come in at a respective 10% and 20% this year, Lee added.

“Going forward, the uncertainties on the external front including but not limited to the Russia-Ukraine war and the pace of interest rate normalisation in advanced economies could heighten volatilities in financial markets.

“These will exert pressure on the bottom lines of life insurers in 2022, even with our NB growth expectation and in-force business holding its ground,” she added.